No, it’s a thing idiots should avoid at all costs.

A card with a 2% reward across the board(Fidelity for instance) can be used as a proxy for your debit card week to week.

It builds my credit, gives me a group of attack dogs to sic on anyone who rips me off, and gives me a cushion if I ever need it. If you never exceed your expenses and never reach beyond your means, it’s no different in consequence than paying with anything else, with a little added bonus credit and reward.

It’s people and their lack of self control that ruin credit cards.

I would expect a massive nerf/devaluation of rewards if there’s no poor people getting exploited.

I say this as someone who pays for all his family vacations almost entirely with points. About every year and a half. This time was Texas for the eclipse. Before that it was Disney world for my kids 5th birthday. Before that was COVID times and I used my points to buy hardwood floors that I installed throughout my house. Before that it was SC for the eclipse.

While I do feel a sense of involvement in their exploitation by being a part of this system, I’m not going to feel bad for anyone who can’t follow the simple rules of the game.

Where’s the line between exploitation and personal fault? I can’t expect everyone who’s ever owned a credit card to have been put in the same situation where it’s the only way. For all I know, my last reward points trickled down from some asshat who financed a car on unemployment.

Absolutely banks will cut rewards, I know that when there was a law attempting to cap/eliminate late fees banks I am close to were discussing how they would offset the losses and rewards were on the block for that. That law is held up in Texas courts right now so the banks so far haven’t had to worry about it

Considering how many Americans have crippling credit card debt, especially poor people, would that be worse? I’m sure they’d still offer those credit builder cards with low limits that you have to deposit collateral for the limit.

I’d expect a lot more use of buy now pay later schemes like Klarna.

It’s similar to a credit card, but prevents build up of crippling debt.

I personally use my credit card and pay in full each month, not because I need the credit, but because in the UK you get the benefit of Section 75 protection on purchases. I’ve used that a few times when companies have gone bust. If I’d paid on debit card I’d have been screwed.

Buy now, pay later does not prevent crippling debt. It makes it easy to buy without thinking or realising the actual cost. It makes is easy to stack up invoices that you in the end can’t afford.

Don’t Americans have a thing called Credit Score. If you are not paying off debt you don’t build up a score and good luck getting a mortgage without one.

Credit balances don’t negatively impact credit scores as much as one would think. It’s ultimately a combination of factors that go into an overall credit score with the heaviest hitter being payment history. If one makes all of their payments they can have a decent credit score despite carrying a 10k balance. Carrying a balance of greater than 30% of the limit will detract significantly from the overall score, but it won’t knock it below “decent” range on its own.

I’m honestly not even sure how one actually gets their score below 500. My wife got a head injury and physically could not remember whether or not she’d paid her credit cards a couple of years ago, so they ended up becoming delinquent and going to collections. Ultimately it dropped her credit score to about 500 but then it started climbing back up from the car loan and mortgage that are in both of our names and is almost up to 700 again. I seriously want to know how people manage to get their scores down to the 300s (the floor is 300) because you basically have to try in order to get your score that low. A friend of a colleague managed such a feet and then had some identity theft which actually improved his credit score because it looked more like normal credit activity than his real credit activity

It’s a combination of factors. Having debt itself isn’t as important as payment history, age of accounts, etc. Credit card debt is probably the opposite of helpful; paying off a card every month in full for a long time is much more useful.

Actually asking, not rhetorical: if poor people are already getting charged based on what they can afford, would this policy exert a downward force on prices?

So way less financing options, slightly more buying outright?

Sure, if we presuppose that credit cards exist as a way for a middleman company to make a huge profit and pay their CEO tens of millions of dollars annually. If we instead consider them a regulatable utility, the necessary rates for viable operation go pretty far down. The business model of “convenience is free or even costs less than cash for those who already have plenty, and this convenience is funded by the destitute who are being held down by the exact same people” is also suspect to begin with, and I’d rather DiSrUpT tHe EcOnOmY than remain complicit, which I am

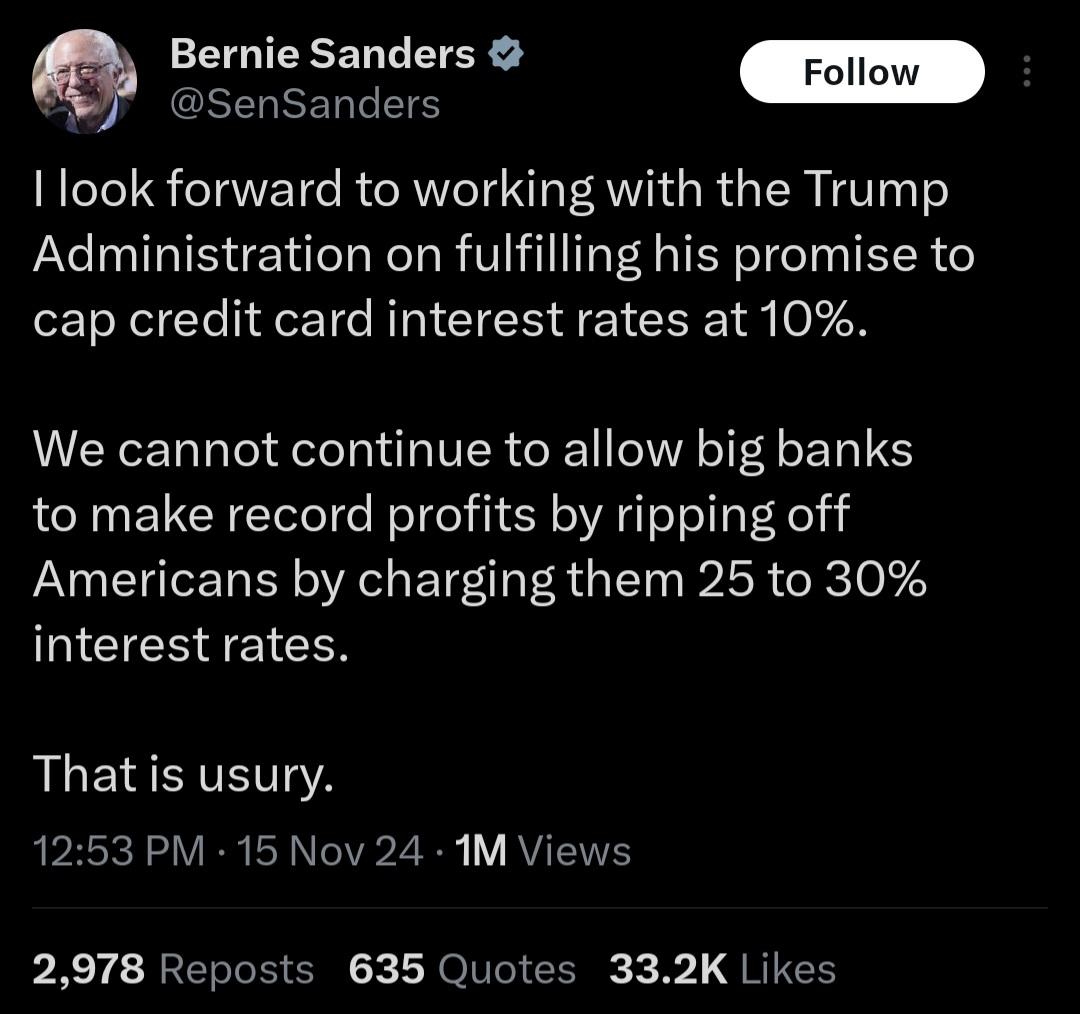

{kind=link}

What that would actually mean is a complete lock-out on credit cards for the poor.

I don’t see that as a real problem. Because as it is now, credit cards are something poor people should avoid at all costs.

No, it’s a thing idiots should avoid at all costs.

A card with a 2% reward across the board(Fidelity for instance) can be used as a proxy for your debit card week to week.

It builds my credit, gives me a group of attack dogs to sic on anyone who rips me off, and gives me a cushion if I ever need it. If you never exceed your expenses and never reach beyond your means, it’s no different in consequence than paying with anything else, with a little added bonus credit and reward.

It’s people and their lack of self control that ruin credit cards.

I would expect a massive nerf/devaluation of rewards if there’s no poor people getting exploited.

I say this as someone who pays for all his family vacations almost entirely with points. About every year and a half. This time was Texas for the eclipse. Before that it was Disney world for my kids 5th birthday. Before that was COVID times and I used my points to buy hardwood floors that I installed throughout my house. Before that it was SC for the eclipse.

While I do feel a sense of involvement in their exploitation by being a part of this system, I’m not going to feel bad for anyone who can’t follow the simple rules of the game.

Where’s the line between exploitation and personal fault? I can’t expect everyone who’s ever owned a credit card to have been put in the same situation where it’s the only way. For all I know, my last reward points trickled down from some asshat who financed a car on unemployment.

Absolutely banks will cut rewards, I know that when there was a law attempting to cap/eliminate late fees banks I am close to were discussing how they would offset the losses and rewards were on the block for that. That law is held up in Texas courts right now so the banks so far haven’t had to worry about it

deleted by creator

Considering how many Americans have crippling credit card debt, especially poor people, would that be worse? I’m sure they’d still offer those credit builder cards with low limits that you have to deposit collateral for the limit.

I’d expect a lot more use of buy now pay later schemes like Klarna.

It’s similar to a credit card, but prevents build up of crippling debt.

I personally use my credit card and pay in full each month, not because I need the credit, but because in the UK you get the benefit of Section 75 protection on purchases. I’ve used that a few times when companies have gone bust. If I’d paid on debit card I’d have been screwed.

Buy now, pay later does not prevent crippling debt. It makes it easy to buy without thinking or realising the actual cost. It makes is easy to stack up invoices that you in the end can’t afford.

Don’t Americans have a thing called Credit Score. If you are not paying off debt you don’t build up a score and good luck getting a mortgage without one.

Credit balances don’t negatively impact credit scores as much as one would think. It’s ultimately a combination of factors that go into an overall credit score with the heaviest hitter being payment history. If one makes all of their payments they can have a decent credit score despite carrying a 10k balance. Carrying a balance of greater than 30% of the limit will detract significantly from the overall score, but it won’t knock it below “decent” range on its own.

I’m honestly not even sure how one actually gets their score below 500. My wife got a head injury and physically could not remember whether or not she’d paid her credit cards a couple of years ago, so they ended up becoming delinquent and going to collections. Ultimately it dropped her credit score to about 500 but then it started climbing back up from the car loan and mortgage that are in both of our names and is almost up to 700 again. I seriously want to know how people manage to get their scores down to the 300s (the floor is 300) because you basically have to try in order to get your score that low. A friend of a colleague managed such a feet and then had some identity theft which actually improved his credit score because it looked more like normal credit activity than his real credit activity

It’s a combination of factors. Having debt itself isn’t as important as payment history, age of accounts, etc. Credit card debt is probably the opposite of helpful; paying off a card every month in full for a long time is much more useful.

Actually asking, not rhetorical: if poor people are already getting charged based on what they can afford, would this policy exert a downward force on prices?

So way less financing options, slightly more buying outright?

Problem is the assumption that prices would go down if some people cannot afford it.

Whats happening instead is people going hungry and homeless.

The reason for this is that Supply:Demand Equilibrium is further up in price range where fewer sales at higher value yields the maximum profit.

Sure, if we presuppose that credit cards exist as a way for a middleman company to make a huge profit and pay their CEO tens of millions of dollars annually. If we instead consider them a regulatable utility, the necessary rates for viable operation go pretty far down. The business model of “convenience is free or even costs less than cash for those who already have plenty, and this convenience is funded by the destitute who are being held down by the exact same people” is also suspect to begin with, and I’d rather DiSrUpT tHe EcOnOmY than remain complicit, which I am

Doubt.